Loading...

Find thousands in tax deductions in as little as 30 seconds

Connect your card to Everlance and tell us what you do for a living. Proudly powered by Plaid, Everlance supports connections with over 20,000+ institutions.

Within 30 seconds our technology will scan your transactions for potential tax deductions. Review the list of expenses and remove the personal expenses.

We'll build an expense log for you in IRS-compliant reporting. Watch your deductions add up through the year and save big at tax time!

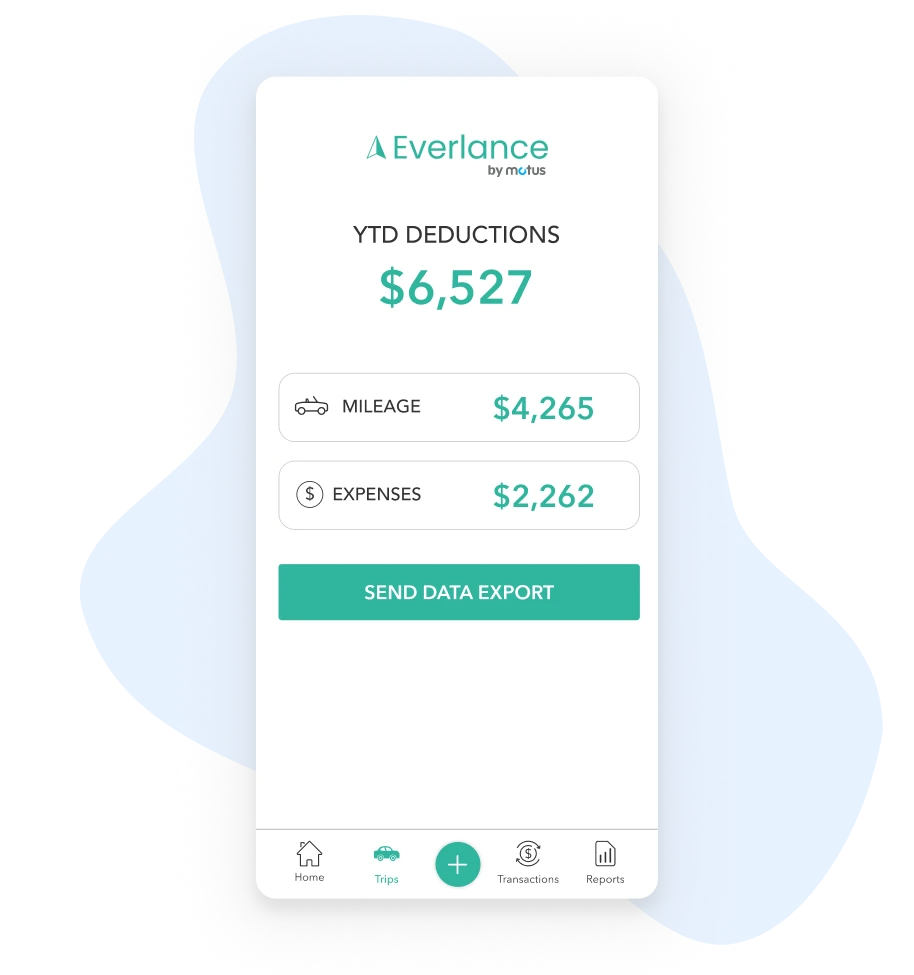

Everlance is built with your all your potential deductions in mind. Not only can you track all your work expenses through our deduction finder but you can automatically track every mile with our award winning automatic mileage tracker.

Yes! Professional plans come default with a 7 day free trial, giving you unlimited access to expense tracking, deduction finder, tax filing, and other tools to make self-employment a breeze.

We take security very seriously here at Everlance. We use 256 Bit Encryption on all of our data and tokenize and encrypt sensitive data and advocate for the broader use of these protocols throughout the industry.

The Everlance app is a read-only application and does not store any login info so your data is your data. If you have further questions please contact us at support@everlance.com and we would love to answer any more questions.

Yes, Everlance was not only built for freelancers & independent contractors but also for small and large business alike. There are many companies that use Everlance for expense tracking, reimbursements and employee tax purposes.

.svg)