Mileage Tracker for Insurance Agents every client visit counted. every deduction captured.

Every policyholder visit, prospect meeting, and claims drive is a qualifying business mile. A mileage tracker for insurance agents captures each one automatically, so your log stays complete for tax filing or reimbursement.

$7,200+

20,000+

30%

4.8/5

Miles, policies, and write-offs: the insurance agent's practical guide to mileage tracking

Insurance is a relationship business built on in-person contact. Every renewal appointment, claim walkthrough, and carrier meeting generates business miles with direct financial value on Schedule C or under a broker reimbursement plan. The miles are accumulating. The only question is whether they are being recorded.

What is a mileage tracker for insurance agents and why does it matter?

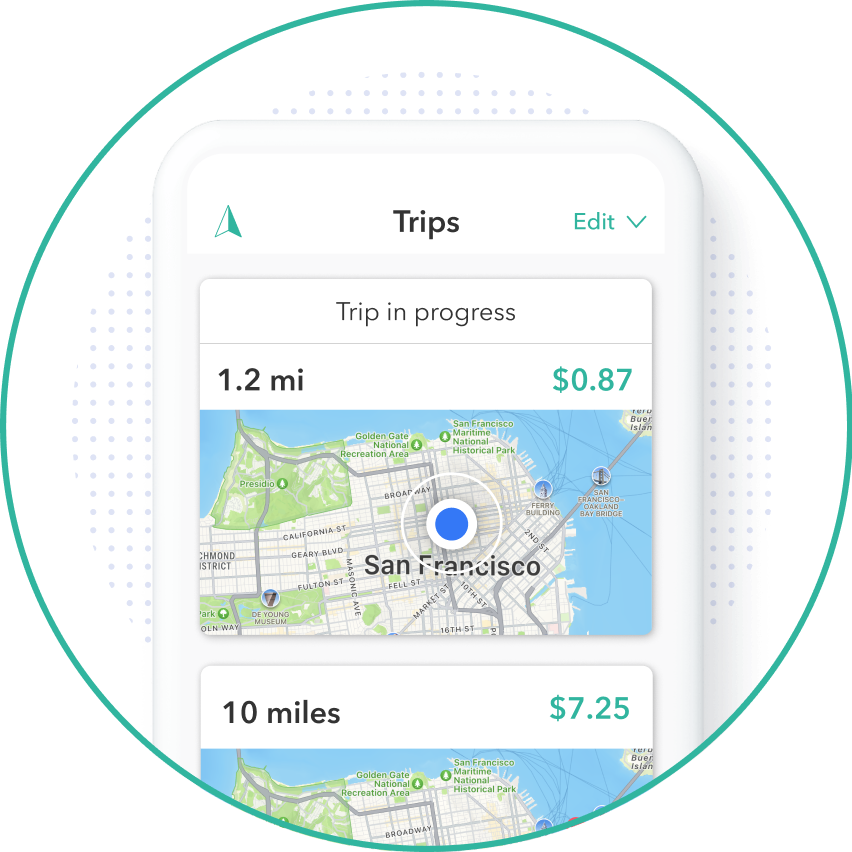

A mileage tracker for insurance agents records every business mile driven across client appointments, policy renewals, claims inspections, and carrier meetings, capturing the date, locations, distance, and purpose of each trip in an IRS-compliant format.

For real estate agents and Realtors, this matters more than in most professions. The nature of the job means you spend a significant portion of your working life behind the wheel — and a well-configured Realtor mileage tracker pays for itself many times over. Client showings, listing appointments, open houses, neighborhood canvassing, broker meetings, and title company visits all rack up miles fast. At the IRS standard mileage rate — which applies to every qualifying business drive — those trips can translate into tens of thousands of dollars in legitimate vehicle expense deductions, money that reduces your taxable income and lowers your tax bill directly.

The reason most agents leave that money on the table isn't lack of eligibility. It's lack of documentation. Without a proper log, even 100% legitimate business trips can be disallowed in an audit. The IRS requires what they call contemporaneous records — meaning trips logged at the time they happen, not reconstructed later from memory or a calendar.

This is where a dedicated mileage log app transforms your workflow. Instead of manually writing down odometer readings or piecing together a real estate agent mileage log from memory each April, your phone does the work in the background — capturing every drive with GPS precision the moment your car starts moving. The best mileage tracker for real estate agents runs silently, requires zero manual input, and hands you an IRS-ready report when it's time to file.

How an automatic mileage tracker works for real estate agents?

An automatic GPS mileage tracker uses the location hardware already built into your smartphone to detect when you start and stop driving — without you needing to press a single button. For agents who are constantly moving between properties, offices, and clients, this is the difference between capturing every deductible mile and losing track of them entirely. Unlike manual methods, a real estate mileage app creates contemporaneous records automatically — exactly what the IRS requires.

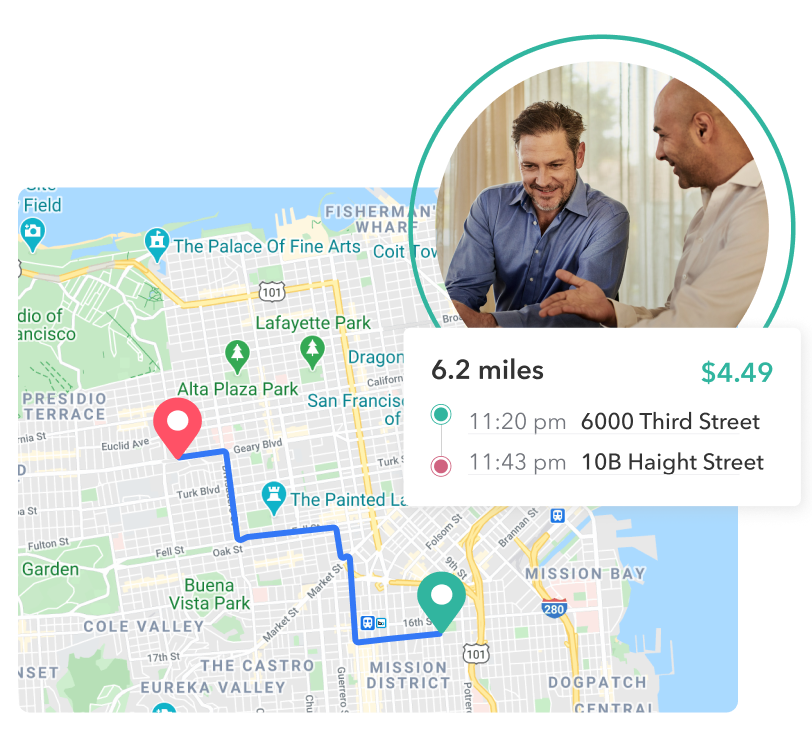

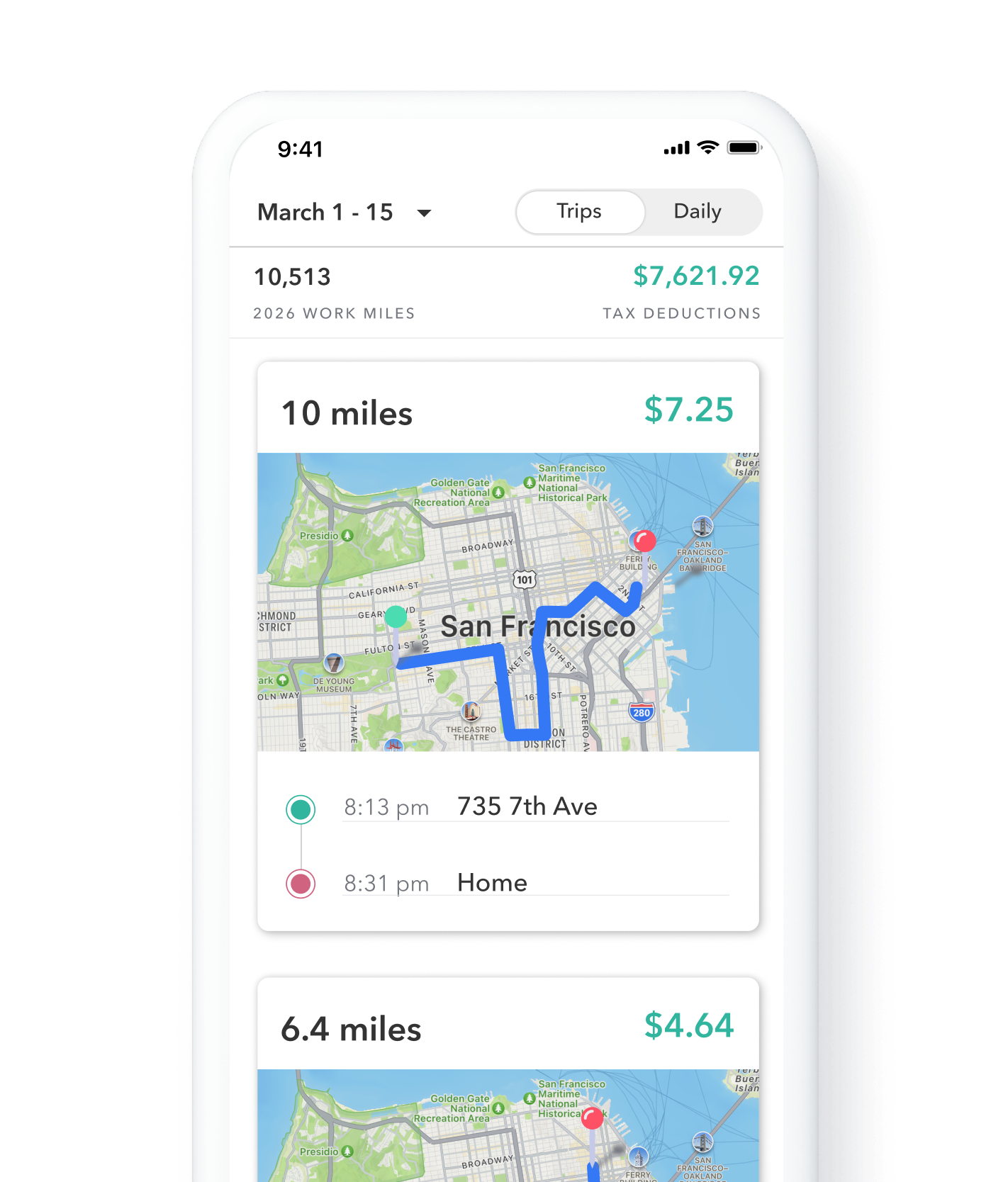

From the first client call to the last renewal visit: see what your mileage is actually worth

See what automatic mileage tracking looks like for an insurance agent in the field, and what your annual deduction or reimbursement could be. Adjust the sliders to match your actual driving volume.

Mileage Savings Calculator

Your 2026 mileage savings estimate

$6,960

Based on IRS standard mileage rate

Insurance agents drive more qualifying miles than most professions. Almost none of them are fully captured.

Most professions have a fixed commute. Real estate agents have a different destination every hour. That constant movement is your biggest untapped tax asset - and the agent mileage deduction is one of the largest line items available to any self-employed professional. The question isn't whether you qualify. It's whether you're capturing it properly.

Your agency management system records policies. It does not record mileage.

Every drive between policyholders carries a defined dollar value at the current IRS rate

Renewal cycles and seasonal claim surges create driving patterns that are impossible to reconstruct

Insurance professionals who track every mile protect their income and remain audit-ready year round

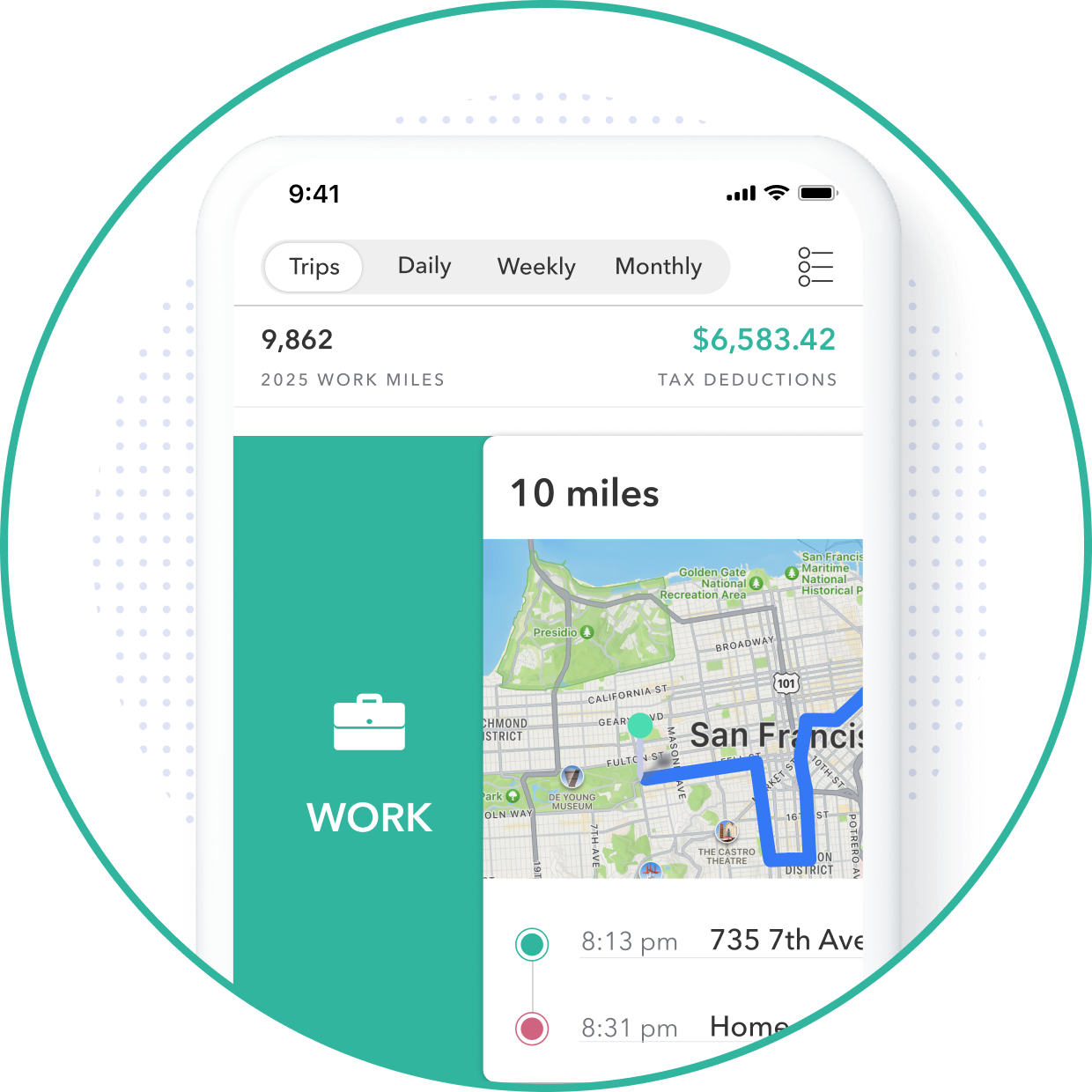

Professionals using automatic GPS tracking capture 30% more deductible miles than those relying on manual logs. For an agent driving 20,000 business miles annually, that gap means thousands in forfeited deductions each year. Manual tracking fails because the workday never pauses long enough to log each drive accurately. Automatic tracking closes that gap entirely. Every drive is captured, every location is GPS-verified, and the log stays current without changing how the agent works.

Qualifying trip types:

Property showings — each leg is a separate deductible trip

Listing appointments and CMA presentations

Open house setup, signage, and hosting runs

Neighborhood farming and prospecting drives

Client meetings at any location

Home inspections, appraisals, and photo shoots

Continuing education and broker training

Title company, lender, and escrow visits

Qualifying trip types for insurance agents

How the IRS treats mileage for independent insurance agents and what it means for your Schedule C

Independent insurance agents deduct vehicle miles on Schedule C, reducing net income before both income and self-employment tax. Every qualifying mile therefore reduces two taxes simultaneously. Captive W-2 agents may instead receive reimbursement through an employer accountable plan. In both cases, the quality of the mileage log determines how much of that benefit is actually captured.

The IRS standard mileage rate for insurance agents: the right method for most

Insurance agents can deduct vehicle expenses using either the IRS standard mileage rate or the actual expense method. For most agents, the standard rate produces a larger deduction with far less administrative complexity.

Under this method, total qualifying business miles are multiplied by the IRS-published rate, which covers fuel, depreciation, insurance, and maintenance in a single figure. A compliant mileage log is the only record required. No fuel receipts or service records are needed.

One critical rule: the standard mileage rate must be elected in the first year the vehicle is placed in service for business. Starting with actual expenses locks the agent into that method for that vehicle. Establishing a mileage log from the first business drive preserves the election.

Agents operating through S-corporations, LLCs, or receiving carrier car allowances should consult a tax professional, as vehicle expense treatment varies significantly by entity structure.

Updated each year by the IRS

Covers gas, insurance, depreciation & maintenance. Applies to all qualifying business miles driven by insurance agents using a personal vehicle.

An agent averaging 380 business miles per week accumulates roughly 19,000 miles annually. At the current IRS standard rate, that volume produces one of the most significant deductions available to any self-employed insurance professional. Every mile that goes unlogged is permanently forfeited with no mechanism to recover it.

Mileage reimbursement for insurance agents: what different agency structures require and how documentation protects you

Insurance agents work under varying compensation structures, from 1099 independent brokers to captive W-2 agents with employer expense plans. Regardless of structure, the documentation standard is the same: contemporaneous trip-level records with dates, locations, distances, and business purposes. Accurate logs produce full reimbursements. Incomplete ones leave money unclaimed.

Independent agents and brokers on 1099 arrangements handle vehicle expenses entirely on their own, deducting mileage on Schedule C. For these agents, the mileage log is the sole basis for any deduction.

Captive W-2 agents may be reimbursed by a carrier or general agency under an accountable plan, where documented mileage is reimbursed at or below the IRS rate and excluded from taxable income. Reimbursements lacking proper documentation are treated as taxable wages.

Fixed car allowances from general agencies or insurance marketing organizations are included in taxable income unless structured as accountable plan reimbursements with a mileage documentation requirement.

In every arrangement, the mileage log is what makes the reimbursement or deduction possible. Without it, no business driving generates a financial benefit that can be claimed.

IRS Compliance Checklist

Date of the trip

Every entry requires a specific date. Weekly or monthly summaries do not meet IRS substantiation standards.

Starting & ending location

GPS-verified coordinates provide objective, timestamped evidence that carries substantially more weight than address-based manual entries.

Total miles per trip

Automatic GPS calculation eliminates the rounding and estimation that commonly draw scrutiny in employer reviews and IRS examinations.

Specific business purpose

Entries like "annual policy renewal, personal lines client" satisfy the IRS requirement. Generic labels like "client" or "insurance" do not.

What insurance agents need to know about mileage compliance

Your agency management system is not a substitute for a mileage log

Agency platforms confirm that appointments occurred. They do not record miles, routes, or GPS coordinates. A dedicated mileage tracking app creates the contemporaneous documentation that no agency system can replicate.

Multi-line and multi-carrier agents need unified tracking across all activity

Agents receiving fixed car allowances often assume documentation is not required. For those payments to qualify as tax-free reimbursements rather than taxable compensation, a compliant mileage log must still be submitted under an accountable plan.

IRS-compliant report format for Schedule C and employer submissions

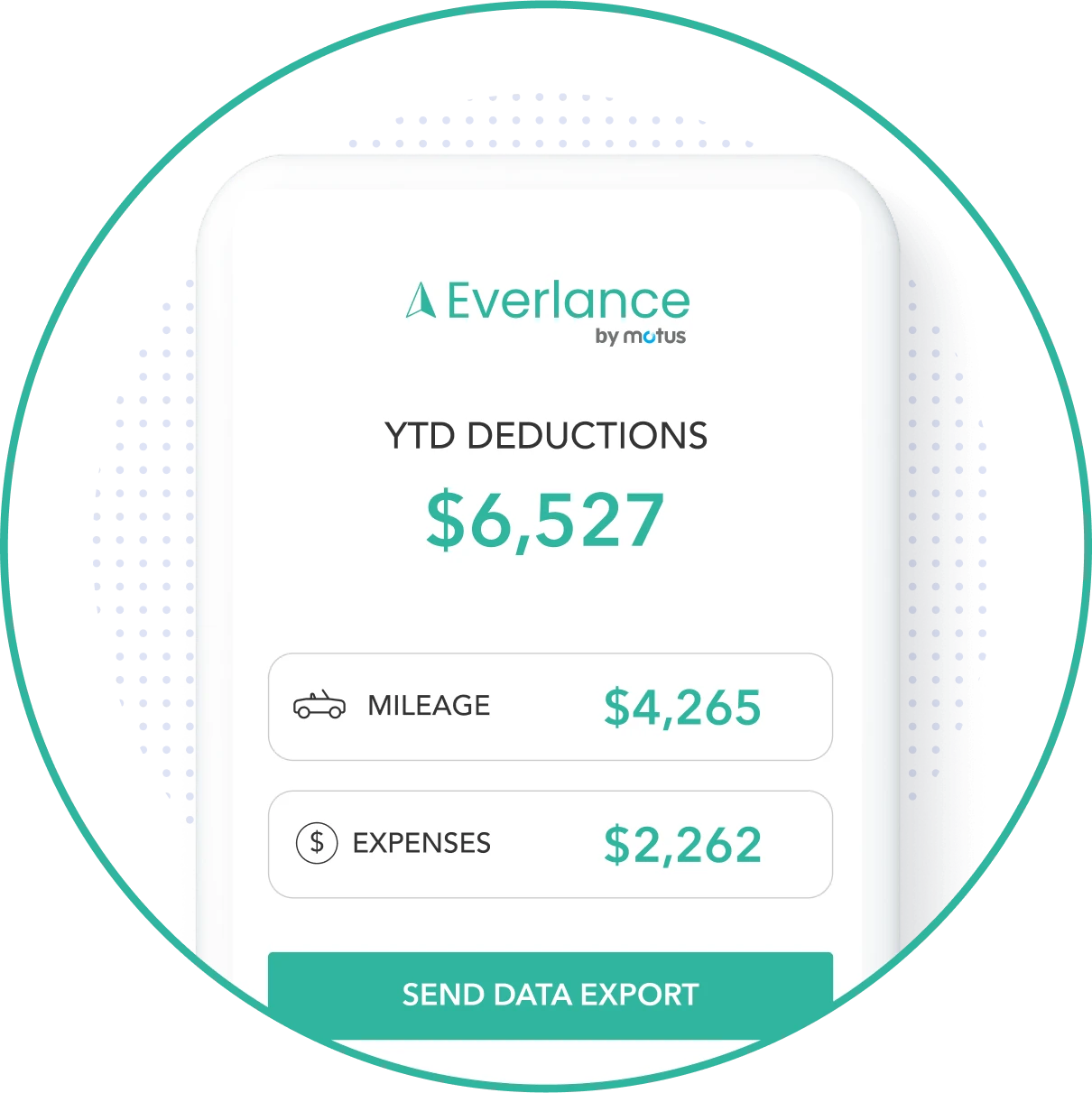

Export IRS Publication 463-compliant mileage reports in PDF, Excel, or CSV, ready for annual tax filing or monthly reimbursement submissions, with every required field included and no additional data entry needed.

Carrier and broker car allowances still require documentation in most arrangements

Agents receiving fixed car allowances often assume documentation is not required. For those payments to qualify as tax-free reimbursements rather than taxable compensation, a compliant mileage log must still be submitted under an accountable plan.

Audit protection for independent agents and 1099 insurance professionals

For 1099 agents deducting vehicle expenses on Schedule C, a GPS-verified mileage log is the strongest available documentation in any IRS examination. Reconstructed estimates from calendars or carrier records carry far less evidentiary weight.

Mileage tracking FAQs for real estate agents

Practical answers to the questions agents ask most. For advice specific to your tax situation, always consult a qualified CPA or tax professional.

.svg)

Still have questions?

Your client drives deserve automatic GPS mile tracking.

Every client appointment and territory drive logged automatically via GPS. Tax and reimbursement ready.